- In a year that was characterized by a decrease in the number of small-cap listings and an increase in the level of selectivity across exchanges, KuCoin’s posture represents a balanced listing distribution.

- It is possible to describe the most important changes that KuCoin will experience in 2025 along three parallel trajectories.

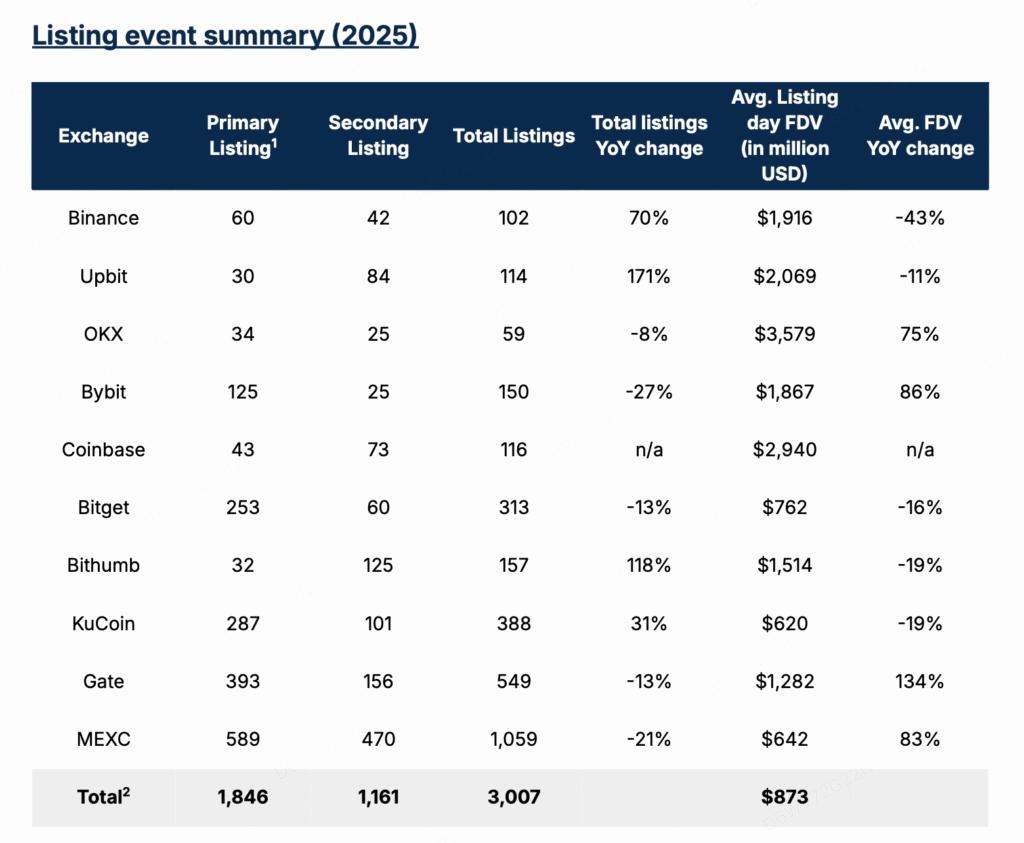

The 2025 Exchange Listing Report has been published by Animoca Brands Research. This report provides an in-depth examination of the ways in which centralized exchanges (CEXs) are adjusting their listing strategy in response to changing market circumstances. The report investigates the dynamics of exchange listing across RWAs and Altcoins, as well as the development of Alpha Programs and new iterations of IDO models. These topics, taken together, provide an overview of how exchange competition in 2025 is becoming more structurally diverse.

In 2025, KuCoin was listed among the top three exchanges in terms of primary token listings, as stated in the report. Additionally, it maintains a considerable listing share within the range of $30 million to more than $500 million in FDV and is among the top platforms in terms of the volume of trade in tokenized gold (RWA). In a year that was characterized by a decrease in the number of small-cap listings and an increase in the level of selectivity across exchanges, KuCoin’s posture represents a balanced listing distribution. It encompasses early-stage projects while maintaining exposure to mid-cap and large-cap assets.

I. Primary token listing activity trending upward

According to the Animoca Brands Listing Report, KuCoin placed among the top three exchanges in 2025 in terms of the number of token listings. This is a 31% increase from the previous year. It is stated quite clearly in the research that “KuCoin has demonstrated strong activity in primary token listings.”

This discovery results in two different implications. In a capital climate that is increasingly selective, main listing is a statement of the strength of upstream transactions flow and the potential to acquire projects. The capacity to maintain primary market activity requires both competitive access to rising projects and trust in internal vetting frameworks. This is because major exchanges are adopting more stringent listing requirements.

A important aspect is the market share of the listing. Within the range of 30 million to 500 million or more FDV, KuCoin maintains a significant percentage. A very selective approach is shown in the fact that “Top-tier exchanges” are responsible for twenty-five percent of listings in the “heavyweight” category at a value of more than five hundred million dollars. Within this paradigm, the fact that KuCoin is able to keep a consistent share in the mid- to large-cap valuation tiers indicates that the project coverage across value strata is generally balanced.

II. Liquidity Efficiency

If we look at the data from 2025 and 2024, we can see that there has been a significant change in the structure of the market’s liquidity. In comparison to 2024, the initial 24-hour trading volume of micro-cap projects (representing less than 30 million FDV) and small-cap projects (representing 30 million to 100 million FDV) decreased. On the other hand, the first-day trading volume of mid- to large-cap projects (with an FDV more than $100 million) had a considerable increase, reaching 1.44x to 1.78x the average for 2024. All of the valuation tiers experienced year-over-year growth on the basis of 30-day trading volume, with the 100M–500M FDV sector having the fastest gain at 2.12 times the average for 2024.

According to these numbers, there has been a structural shift in the preferences of the market. KuCoin’s footprint is aligned with this liquidity shift, which is due to the fact that risk appetite is converging around projects that have higher capitalization and clearer fundamentals. Exchanges that are situated inside these valuation ranges are fundamentally better positioned to capture persistent trade velocity rather than transitory surges. This is because capital is concentrating on listings of higher quality.

III. RWA deployment

One of the most significant subsectors is tokenized gold, which has emerged as a major strategic allocation direction for CEXs. RWA has emerged as a key strategic allocation direction. The report makes the observation that, in the midst of geopolitical concerns and shifting circumstances in macroeconomic policy, gold has become more appealing inside the investment portfolios of traditional financial institutions (TradFi), a trend that has simultaneously spread to on-chain marketplaces. In this particular market, KuCoin is ranked fifth in terms of the volume of trade in tokenized gold.

It is not the short-term explosive growth of Tokenized Gold that is the primary source of its value from a structural standpoint; rather, it is the provision of an on-chain hedging instrument against macro uncertainty, the reinforcement of the “safe-haven” characteristics of an exchange’s asset structure, and the provision of a bridge between traditional financial services capital and on-chain assets.

The fact that KuCoin is participating in this sector demonstrates the amount of importance it places on diversifying its asset structure during periods of extreme volatility.

It is possible to describe the most important changes that KuCoin will experience in 2025 along three parallel trajectories: first, an increase in the amount of primary listing activities; second, the maintenance of a significant share within the mid- to large-cap FDV tiers; and third, the establishment of consistent involvement in RWAs. The progression of KuCoin’s market positioning may be a microcosm of the industry’s move from an expansion cycle to a period of refined, structurally driven competition.