In today’s digital era, money is evolving fast. From cash transactions to online payments, the way we handle money has drastically changed. As physical cash becomes less common, especially during the COVID-19 pandemic due to hygiene concerns and cash shortages, more people are turning to digital transactions. Since then, banks and financial institutions have done far more transactions online than in-person facilities. Additionally, CBDCs have grabbed significant attention, prompting central banks to recognize their growing importance in the evolving financial sector.

Yes! The Central Bank Digital Currencies (CBDCs) could be the next big leap in the financial world. You might have heard the term but may not be familiar with what CBDCs are or how they work. This article will break it down simply and explain why the CBDC future could have a big impact on how we use money.

What Are CBDCs?

At the core, a Central Bank Digital Currency is a digital version of a country’s official currency, issued by the central bank. So, if any country were to launch a CBDC, it would be a digital form of their currency. This isn’t like cryptocurrencies such as Bitcoin or Ethereum, which are decentralized. A CBDC would be completely controlled and regulated by the central bank of the country such as the Federal Reserve in the case of the United States.

CBDCs aim to combine the convenience of digital money (like Paytm or Google Pay) with the safety and reliability of cash since it would be backed by the government. Unlike cryptocurrencies, which can fluctuate in value wildly, a CBDC would hold a stable value, equal to the regular currency.

The Two Types of CBDCs

CBDCs come in two primary forms:

- Retail CBDCs: These are created for general public use (everyday use), in the same way, how we use cash or online payment in the apps today. A retail CBDC will allow individuals to hold digital currencies directly from the central banks.

- Wholesale CBDCs: These are intended for use by a financial institution, banks, and businesses. Wholesale CBDCs could be used for settling large transactions, particularly between banks, more efficiently and securely than the current systems.

Why Do Countries Want CBDC?

There are several reasons why countries across the world are looking into CBDCs:

CBDCs have various benefits, particularly for nations that prioritize financial inclusion like China and India. The financial system might help millions of people access CBDCs without traditional banking facilities with only a mobile phone and internet connection. Additionally, Central Bank Digital Currencies pledge faster and cheaper transactions–especially for cross-border payments.

Fighting Fraud and Black Money for a Stronger Economy: CBDCs traceability could help the government to combat fraud and black money circulation. This feature makes it easier for them to crack down on illicit activities. Central banks can also use CBDCs to boost economic stability by having more control over the money supply, and only injecting funds when necessary. Finally, while cryptocurrencies like Bitcoin become more and more well-known, CBDCs offer the advantages of digital currencies in a safer, more regulated manner.

How CBDC Could Impact Everyday Life?

Central Bank Digital Currencies could significantly change how we use money in different ways. One primary benefit is that, the initiative will let people to make digital payments without the traditional banks help or payment service providers such as Google Pay. CBDCs will simplify transactions and make them quicker as the central banks by issuing currency directly to individuals.

Further, CBDCs will have central bank security features. That will lead them to be much less prone to hacking and fraud as compared to cryptocurrencies and other online payment systems. The transparency of the digital ledger used for CBDCs would enhance their protection. For governments, the traceability of CBDCs could offer clearer insights into monetary activities. This can lead to more informed and effective policy-making. Businesses, in particular small enterprises, could also benefit from lower transaction charges when CBDCs reduce or eliminate intermediary costs. This will ultimately lowering costs for both businesses and consumers.

The Growth of CBDC

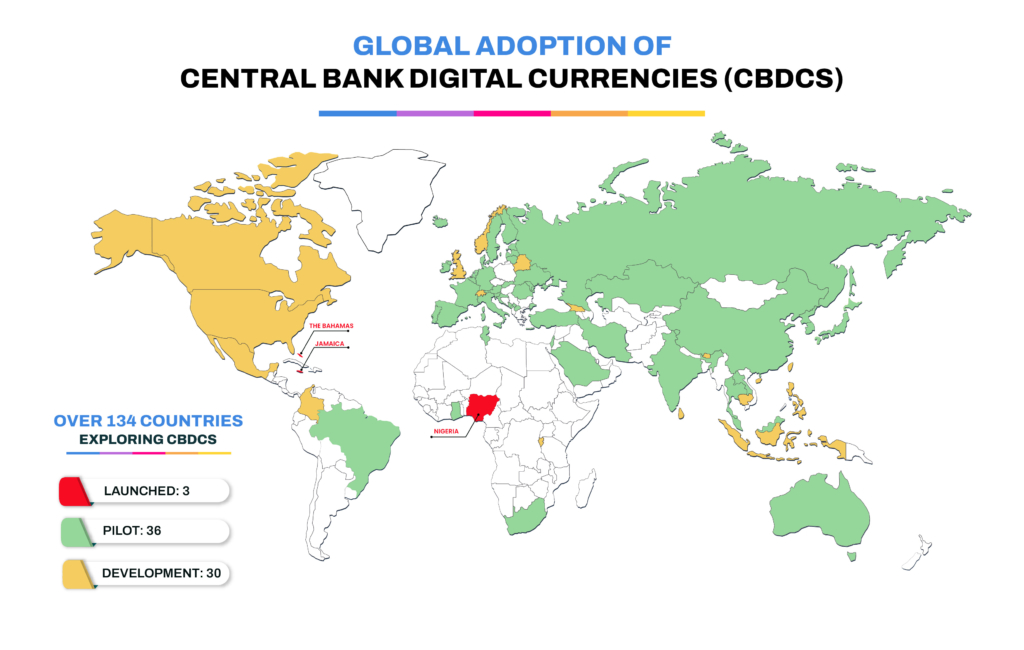

The adoption and exploration of CBDCs have grown significantly in recent years. Around 134 countries and currency unions, which represent 98% of global GDP, are exploring or developing a CBDC, as per the Atlantic Council’s CBDC tracker (as of May 2024). This is a sharp increase from only 35 countries just four years ago in 2020.

Among the Group of 20 (G20) countries, 19 nations are already in advanced stages of CBDC development. 11 countries—including Brazil, Japan, India, Australia, South Korea, South Africa, Russia, and Turkey—already in the pilot stage. Further, several nations—like Nigeria, Jamaica, and The Bahamas—have fully implemented the CBDCs. For example, China’s digital yuan (e-CNY) has become the world’s largest CBDC trial. Over 260 million wallets being used across 25 locations.

CBDCs are also gaining popularity in the international payment sector. The BRICS countries like Brazil, Russia, India, China, and South Africa are exploring CBDCs not only for retail but also for large-scale wholesale payments across borders, planning to reduce reliance on the US dollar for international trade. CBDC projects like mBridge are already testing international transactions between countries like China, Thailand, Hong Kong, and the UAE.

While the United States has lagged in this zone, with progress on retail CBDCs stalling, other G7 economies like the UK and Japan continue to move forward with their CBDC explorations.

Challenges and Concerns

While CBDCs offer plenty of benefits, some difficulties remain that the government needs to be tackled. Privacy is a big concern since digital transactions can be tracked, making people worry about being monitored too closely. Then there’s cybersecurity – with more digital money in use, the risk of hacking goes up, so strong protection systems are a must. Another issue is technology. The countries which developing the CBDC will require a good infrastructure, yet rural parts in some continue struggling with insufficient internet access. Finally, the rise of CBDCs may have an influence on traditional banks, possibly lowering their income from fees and interest, leading to larger economic effects.

How CBDCs Are Performing in Practice?

CBDCs could pose serious risks to financial privacy by centralizing transactions with the government, much like the Bank Secrecy Act. This could be the biggest threat to financial privacy. While some say CBDCs are still theoretical, over billions of people are living in countries where they’ve already been launched, including China, the Bahamas, Nigeria, and several Caribbean nations. Yet, most people don’t know what CBDC is or if their government is considering one.

While some believe CBDCs could help the unbanked, many people without bank accounts say they prefer to keep their privacy, as per recent surveys. With trust in government at historic lows and financial surveillance already mandated by law, it’s unlikely that a CBDC would be a solution for these people. This skepticism isn’t just theoretical. In countries where CBDCs have already been launched, public interest and usage have been very low. In places like the Caribbean, China, and the Bahamas, governments have tried various methods to encourage the use of CBDCs, including giveaways, discounts, and loyalty programs.

People in these countries sticking with options like mobile banking and cash instead. Some governments have even taken more extreme measures to push CBDC adoption. In Nigeria, for example, the government triggered a cash shortage in an attempt to get more citizens to use its CBDC, despite the fact that less than 0.5% of Nigerians were using it.

In the Bahamas, the government is soon expected to mandate that commercial banks distribute its CBDC. Meanwhile, in Thailand, the government launched a quasi-CBDC through a digital wallet that restricts payments to specific government-approved goods, only in stores within the district listed on each person’s ID card.

The Possible of Gold-Backed CBDCs

Imagine a future where gold-backed CBDCs become the new standard for digital money. While Central Bank Digital Currencies are currently being explored, gold-backed versions could be a real game-changer. They’d bring together the lasting stability of gold—an asset that existed more than 4 billion years ago—with the convenience of digital currency. In fact, countries like Zimbabwe are already starting to explore this exciting possibility.

Gold-backed CBDCs might offer a more stable and secure way to exchange money, especially during economic uncertainty. They could help businesses protect against inflation and currency fluctuations, and if more countries adopt them, they could lead to a more unified global financial system.

However, like all CBDCs, gold-backed versions would be fully trackable, raising privacy concerns and potential government oversight. Unlike standard CBDCs, which aren’t backed by tangible assets, a gold-backed CBDC could provide more stability because its value is tied to physical gold. But this also means countries would need to maintain large gold reserves, which could impact monetary policy and liquidity during economic downturns.

Conclusion

CBDCs are still in their early phases of development, but it is evident that they will have a significant part in the future of money. Countries around the world are looking into digital currencies as a way to modernize their financial systems, increase payment efficiency, and offer new payment ways for inclusion in finance in the country.

Also, the possibility of gold-backed CBDCs may gain attention, as some nations seek possibilities—we may soon see a new definition of what the future of money is and how it functions in the global economy. Whether fiat-backed or tied to a tangible asset like gold, CBDCs represent a major shift in how we think about and use money.

FAQs

1. What is the security of a CBDC?

CBDCs are traceable and provide transparency in transactions, helping to prevent illicit activities like money laundering. They also simplify cross-border transactions by reducing the complexities of international transfers.

2. How does a CBDC affect the financial sector?

A CBDC can help lower leverage and reduce risks associated with portfolios and assets. It is linked to increased lending, especially in emerging economies. Retail CBDCs tend to promote financial stability, while wholesale CBDCs may have a less positive impact.

3. What are the features of a CBDC?

CBDCs typically offer centralized regulation, ease of use, the ability to handle global transactions, and enhanced security.

4. What is the role of a CBDC in financial inclusion?

CBDCs are liabilities of the central bank and can be made available to all residents, similar to traditional paper currency. This means the country’s money supply would include the total CBDC in circulation.

What are the benefits and risks of a CBDC for banks?

CBDCs can benefit banks by potentially offering a more stable form of money. However, they may also reduce the amount of deposits banks hold, affecting their liquidity and potentially impacting their ability to lend money.